NYC Certificate of Insurance (COI) | The “Scaffold Law” Survival Guide

Why a standard COI will get you kicked off an NYC job site?

In Manhattan or Brooklyn, a “standard” insurance certificate is often just a piece of paper. Because of New York’s Labor Law 240 (The Scaffold Law), NYC is the most expensive place in America to insure a construction project. If your (COI) Certificate of Insurance does not have the specific “magic words” in the Description of Operations. You are not just uninsured, you are a legal target.

The “Additional Insured” Trap

Most generic blogs say “just add the landlord’s name.” That is not enough in New York. To outrank the competition and pass a building manager’s review. Your COI must highlight the “Primary and Non-Contributory” clause.

In a 2026 NYC lawsuit, if your policy isn’t “Primary,” the landlord’s own insurance is forced to pay first. This triggers a legal chain reaction where their insurer sues you to recover those costs.

The Pro Tip: Your COI must explicitly state that your coverage is primary regardless of any other insurance the landlord or GC might carry.

Why NYC Landlords are “COI-Obsessed”

It isn’t just about a leaky pipe or a scratched hallway. NYC landlords are terrified of two things: Local Law 11 (FISP) and Action-Over Claims.

The Danger of “Action-Over” Claims

This is the “hidden” risk that bankrupts NYC contractors. An employee gets hurt, collects Workers’ Comp, and then sues the Landlord for “failing to provide a safe site.” The Landlord then uses the Indemnification Agreement to sue the GC.

Suggestion:

Without an Action-Over Wrap or specific General Liability endorsements (ISO Form CG 20 10). Your COI is worthless against these multi-million dollar “gravity-related” lawsuits.

2026 NYC Limit Standards: Is $1M Enough?

Generic blogs suggest $1,000,000. In 2026, NYC real estate, $1M is the “entry fee,” but it rarely closes the deal for serious work.

| Project Type | General Liability | Umbrella/Excess | Total Protection |

| Interior Reno | $1M / $2M | $1M – $2M | $2M – $4M |

| Exterior/ Structural | $1M / $2M | $5M – $10M | $6M – $12M |

| Luxury Co-op/Condo | $2M / $4M | $10+ | +$12M |

The “Co-op Rule”: Many Upper East Side or Central Park West buildings require GCs to carry at least $5M–$10M in Umbrella coverage just to bring a toolbox through the service entrance.

How to Get a “Bulletproof” COI

Don’t just call a 1-800 number. You need a broker who understands the nuances of the ACORD 25 form in a litigious market.

- The “Per Project” Aggregate: We ensure your limits aren’t being “eaten up” by other jobs you’re doing across the city. Your COI should state the limits apply per project (ISO Form CG 25 03).

At Smart Apple, we use real-time verification to ensure your carrier hasn’t been downgraded by A.M. Best mid-project. If your carrier’s rating drops below an “A-“, most NYC landlords will reject the COI on the spot.

Conclusion:

In a city where a single fall can result in a $10M judgment, your COI is your shield. Smart Apple Insurance Brokers specializes in the high-stakes NYC market. We don’t just “issue certificates”, we build legal fortresses around your business.

FAQs

Does an ACORD 25 prove I have Workers' Comp?

No! In New York, an ACORD 25 is not legal proof of Workers’ Comp. You must provide the C-105.2 or U-26.3 forms specifically.

What is the "Residential Exclusion"?

If you are working on a Condo or Co-op but your policy has a “Residential Construction” exclusion, your insurance won’t pay a dime. We check for this before you sign the contract.

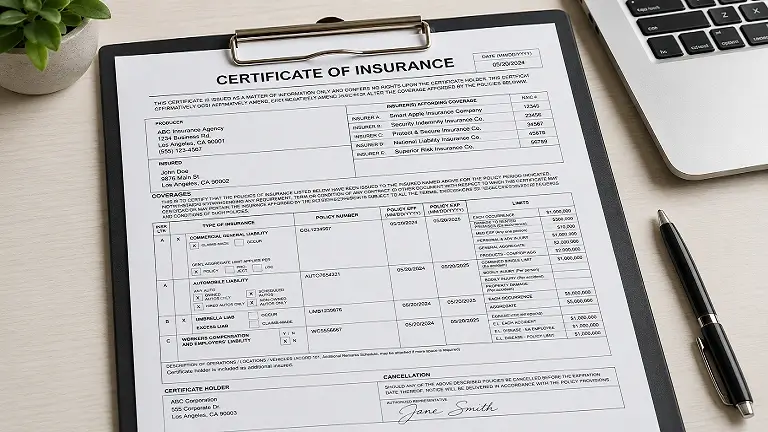

What is the Certificate of Insurance?

A Certificate of Insurance (COI) is a standardized one-page document (usually the ACORD 25 form) that summarizes your active insurance coverage. It is not the policy itself, but a snapshot that proves to landlords and clients that you have the right protection, limits, and dates in place before you step onto a job site.

How do I get a certificate of insurance?

Here is the fastest way to secure a compliant certificate:

- Contact Your Broker: Reach out to your insurance broker or agent with the specific requirements from your contract.

- Provide Details: Give them the Certificate Holder’s name and address, required coverage limits, and any specific “magic words” (like “Primary and Non-Contributory”).

- Download or Receive: Most brokers can issue a COI within a few hours. At Smart Apple, we provide instant digital access and verify that the wording is “bulletproof” for NYC standards before it ever reaches your client.

Alicia Moreau

Alicia F. Moreau is a content writer at Smart Apple Insurance, specializing in clear, engaging, customer-focused insurance content.